KBRA analysis shows software borrowers largely resilient despite rising AI uncertainty and lender caution

KBRA has released an in-depth research report analyzing the evolving impact of artificial intelligence (AI) on software companies and private credit portfolios, offering a nuanced perspective that balances both risk and resilience. As AI continues to reshape industries at an accelerating pace, the report provides a comprehensive evaluation of how this technological transformation is influencing credit risk, lender behavior, and the broader dynamics of private lending markets.

At the core of KBRA’s findings is the conclusion that, while AI introduces new uncertainties, its impact on credit risk within software and technology-focused portfolios remains largely manageable. The agency emphasizes that the risks posed by AI are neither systemic nor immediate in nature. Instead, they are diffuse, unevenly distributed, and likely to materialize gradually over time. This measured view contrasts with more alarmist narratives that portray AI as a near-term disruptor capable of triggering widespread defaults across the software sector.

KBRA’s analysis suggests that most software companies backed by private credit exhibit sufficient adaptability to navigate the challenges and opportunities presented by AI. These firms often benefit from flexible business models, recurring revenue streams, and the capacity to invest in technological innovation. As a result, they are generally well-positioned to incorporate AI into their operations or adjust their strategies in response to competitive pressures. While certain companies—particularly those with structural vulnerabilities or near-term refinancing needs—may face heightened risks, the broader cohort demonstrates resilience.

The report acknowledges that some sponsor-backed borrowers could experience meaningful stress, especially those exposed to rapid technological displacement or operating in highly competitive segments of the software market. These pressures may lead to a modest uptick in default rates. However, KBRA maintains that such outcomes are likely to remain contained within acceptable risk thresholds for direct lending portfolios. Importantly, the agency does not anticipate significant ratings deterioration across its rated entities as a result of AI-related disruptions.

A key theme highlighted in the research is the role of diversification in mitigating potential losses. Even in scenarios where AI-driven stress leads to defaults among higher-risk borrowers, the impact on individual investment vehicles is expected to be limited. Exposure to vulnerable companies is typically spread across a wide range of lenders, funds, and sponsors, reducing concentration risk. This structural characteristic of private credit portfolios serves as a critical buffer against localized disruptions.

Beyond the direct effects of AI, KBRA underscores that macroeconomic conditions represent a more immediate and substantial threat to credit quality. Factors such as persistent inflation, elevated interest rates, geopolitical instability, and ongoing supply chain challenges are identified as primary drivers of near-term risk. In comparison, AI is viewed as a longer-term force whose implications will unfold incrementally rather than abruptly.

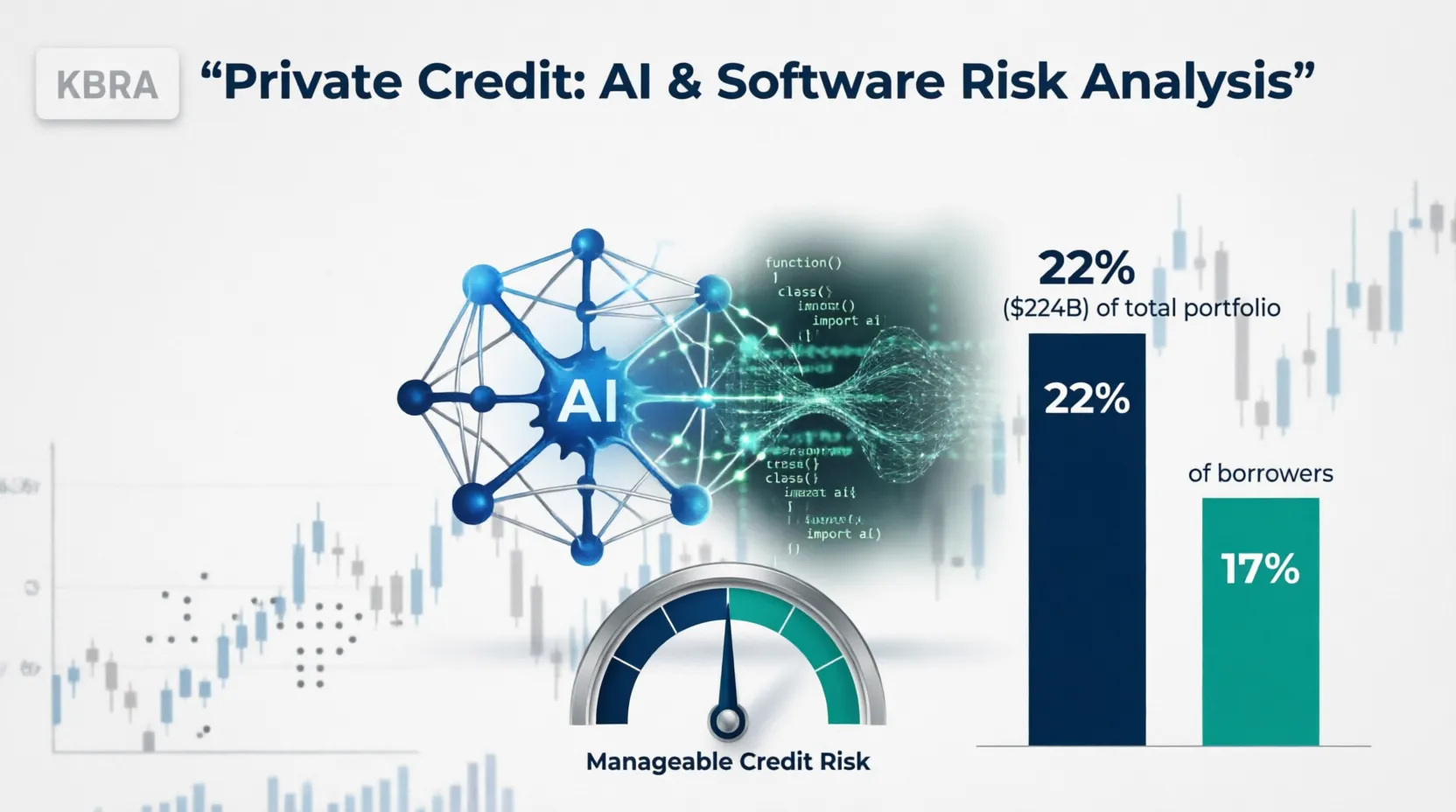

To support its conclusions, KBRA conducted a detailed review of 495 companies within its broader portfolio of more than 2,400 global middle-market borrowers. This subset, categorized as the Software and Technology cohort, includes firms across software, information and telecommunications, and internet and data services sectors. Together, these companies account for approximately one-fifth of the overall portfolio, making them a significant area of focus for assessing AI-related risk.

Within this cohort, KBRA developed a framework to evaluate each company’s relative exposure to AI. This approach considers factors such as business model defensiveness, reliance on legacy technologies, competitive positioning, and capacity for innovation. Particular attention is given to borrowers with near-term debt maturities, as these companies may face greater refinancing challenges in an environment shaped by technological uncertainty.

One of the report’s notable findings is that companies identified as having higher exposure to AI-related risk already exhibit weaker financial profiles compared to their peers. These firms tend to show slower revenue growth, and a larger proportion are experiencing declining sales. In fact, their performance metrics more closely resemble those of traditionally lower-rated sectors such as chemicals, metals, and consumer retail. This pattern suggests that the market may already be pricing in some degree of technological vulnerability, and that lenders and sponsors are actively managing these risks.

The analysis also reveals that a significant share of higher-risk companies faces near-term maturities, defined as obligations coming due before mid-2027. This concentration of refinancing risk underscores the importance of lender discipline and sponsor support in navigating potential challenges. However, even under a hypothetical worst-case scenario in which all such companies default, the overall impact on KBRA’s forward-looking default metrics would remain moderate. This further reinforces the view that AI-related risks are unlikely to trigger systemic disruptions.

Another important dimension of the report is the evolving behavior of lenders and private equity sponsors in response to AI uncertainty. KBRA notes that market participants are already adjusting their strategies, even in the absence of widespread disruption. Lenders, for example, are increasingly incorporating stricter covenants into loan agreements, widening credit spreads, and exercising greater caution when considering maturity extensions. These actions reflect a proactive approach to risk management, aimed at safeguarding portfolios against potential downside scenarios.

Sponsors, meanwhile, are becoming more selective in allocating capital to portfolio companies. Decisions regarding additional investment or balance sheet support are increasingly influenced by assessments of technological resilience and long-term competitiveness. In some cases, uncertainty around AI adoption and its implications for valuation may lead sponsors to delay exits or reduce their willingness to provide incremental funding. This shift in behavior highlights the growing importance of strategic positioning in an AI-driven landscape.

The report also points to early signs of AI’s influence on operating performance within the software sector. While key performance indicators remain broadly stable, subtle changes are emerging. These include shifts in customer purchasing behavior, longer sales cycles, and the reallocation of budgets toward AI-related initiatives. Such trends may contribute to slower growth and margin pressures in the near term, particularly for companies that are slower to adapt or lack the resources to invest in AI capabilities.

Despite these challenges, KBRA maintains a cautiously optimistic outlook. The agency expects that most software companies will be able to adjust to the changing environment, leveraging AI as a tool for innovation rather than viewing it solely as a threat. Over time, the adoption of AI may even enhance productivity, improve operational efficiency, and create new revenue opportunities, ultimately strengthening credit profiles.

From an investment perspective, one of the most significant implications of AI is the increasing dispersion of returns across private credit vehicles. As companies respond differently to technological disruption, performance outcomes are likely to diverge more sharply. This trend underscores the importance of rigorous credit selection, sector expertise, and active portfolio management in achieving favorable risk-adjusted returns.

In conclusion, KBRA’s research provides a comprehensive and balanced assessment of AI’s impact on software and private credit markets. While acknowledging the potential for disruption, the report emphasizes that risks are manageable, gradual, and largely contained within existing frameworks. The combination of diversified portfolios, proactive lender behavior, and adaptive business models positions the sector to withstand the challenges ahead.

At the same time, the findings serve as a reminder that technological change does not occur in isolation. Broader economic conditions, geopolitical developments, and market dynamics will continue to play a critical role in shaping credit outcomes. As such, stakeholders must remain vigilant, integrating both technological and macroeconomic considerations into their decision-making processes.

Source link: https://www.businesswire.com